EU industry leaders warn of strategic vulnerability while US officials unveil financing tools to secure supply chains: Remaining passive is no longer an option. Europe is Late in the Game, discussions at Giga Europe 2026 in Brussels revealed. Europe’s vulnerability is political. But there’s no one-size-fits-all solution. And Europe is still reluctant to pay the Price of Resilience.

A series of discussions in Giga Europe 2026 event in Brussels revealed the emerging geopolitical race for critical minerals that underpin modern energy systems, defence technologies and digital infrastructure. European officials and industry leaders warned that the continent risks falling behind in securing access to these resources, while a senior US government representative presented an industrial policy designed explicitly to finance projects and lock in supply chains for American demand.

Taken together, the discussions illustrated a growing strategic competition between the European Union, the United States and China to secure access to lithium, rare earths, nickel, graphite and other materials essential for batteries, electrification and advanced technologies. Both sides are responding to the same underlying challenge: China’s dominant position in critical mineral extraction and especially processing.

But the approaches are diverging. Europe is still debating how to finance and organise its supply chains. Washington has already begun deploying large public funding programmes to accelerate projects and reshape global mineral value chains.

Raw Materials as a Geopolitical Issue

At the Giga Europe 2026 panel in Brussels, Geert Muylle, Belgium’s ambassador and special envoy for energy security and critical raw materials, argued that the mineral trade has moved beyond traditional market economics and into geopolitical competition.

“What we’ve been observing for several years is that the raw materials business has become as much an affair of government as it is of businesses,” Muylle said.

Some countries now hold dominant positions in particular minerals and processing chains and are willing to “leverage these positions for political purposes”. For European governments, he warned, remaining passive is no longer an option.

“We have no choice as governments but to also enter into this new raw materials business. Because, very simply put, this is about our industrial future.”

Belgium itself hosts roughly 30 midstream processing companies involved in refining, separation and recycling. Together they produce roughly half of the 34 critical raw materials listed by the European Commission, according to Muylle.

But this sector is increasingly under pressure.

“They are squeezed from upstream,” he said, pointing to export restrictions and declining availability of raw materials. At the same time they are “squeezed downstream because many of their clients have still yet not integrated the idea of paying what I call a resilience premium”.

Europe is Late in the Game

Industry representatives echoed concerns that Europe’s policy response remains slow compared with other regions.

“I think Europe is a bit late in the game, to say the least,” said Jonathan Vanherberghen, Director of External Affairs Europe at Rio Tinto.

Other countries have already begun implementing targeted industrial policies. Canada, Australia and the United States have used a mix of public investment, stockpiling agreements and supply partnerships to secure minerals for Western supply chains.

Vanherberghen pointed to a Canadian project involving scandium as an example.

“We’ve done an agreement with the Canadian government on scandium,” he said. The deal combined capital investment, an offtake agreement and a stockpiling arrangement, effectively securing supply for Western markets.

The broader lesson, he argued, is that governments need flexible tools tailored to individual projects and materials.

“There’s no one-size-fits-all solution,” Vanherberghen said. “You need a full toolbox and tailor-made solutions for specific materials, projects and companies.”

Europe’s vulnerability is Political

Vincenzo Conforti, Head of Government Relations Europe at Glencore, offered a stark diagnosis of Europe’s position.

“The vulnerability is more industrial and political than it is geological,” he said.

Europe has strong infrastructure, sophisticated logistics and many of the world’s largest commodity trading houses. Yet it remains structurally dependent in refining capacity and several critical parts of battery and defence supply chains.

Conforti argued that policymakers often misunderstand the issue by treating raw materials as a standalone topic.

“Critical raw materials as such do not really exist. There are only critical value chains, and the minerals that feed these value chains.”

For that reason, the strategic goal should not be complete self-sufficiency but resilient partnerships across trusted countries.

“Replicating every stage of every value chain domestically does not really make a lot of sense,” he said.

Europe is Still Reluctant to Pay the Price of Resilience

A central theme of the discussion was Europe’s hesitation to fund supply chain security.

“We haven’t quite yet accepted that security of supply comes at a price,” Conforti said.

The United States, by contrast, has been moving aggressively, deploying procurement policies and public financing to support mineral processing and battery supply chains.

Vanherberghen observed that many European companies still treat minerals primarily as a purchasing issue rather than a strategic one.

“They look at it purely as a procurement issue, buying at the lowest cost possible,” he said.

That mindset remains a barrier to long-term supply security.

When asked whether customers are willing to pay higher prices to secure alternative supply chains outside China, his answer was blunt.

“I would say not really.”

Recycling Cannot Replace Mining

Recycling is often presented as Europe’s solution to limited mineral resources, but industry experts cautioned against unrealistic expectations.

“Recycling cannot be the alternative to primary materials. It is a complement,” Conforti said.

Even metals such as copper, which has been mined for more than four thousand years, still require substantial primary production to meet global demand.

Recycling also faces practical barriers in Europe.

“It cannot be that it is still easier and cheaper to transport from Germany to Korea than it is to move from Germany to Spain,” Conforti said. “This is the absurdity we’re living in at the moment.”

China’s Dominance Driving Western Policy

Behind the policy debate lies a clear geopolitical concern. China currently dominates several stages of critical mineral supply chains, particularly refining and processing.

“China has established dominant positions in certain extraction activities,” Muylle said.

At the same time, the United States has begun moving aggressively to catch up.

“We’ve seen the activity of the United States trying to catch up with very deep pockets, very fast, very proactively scooping up assets around the globe,” he said.

Europe therefore faces competition from both directions, from China’s established dominance and from an increasingly assertive American strategy.

Washington Arrives with Funding Tools

That American strategy was on full display in Brussels when Widad Whitman, Head of Supply Chain Security for the Office of Critical Minerals and Energy Innovation at the US Department of Energy, outlined Washington’s industrial policy.

“My role focuses primarily at the nexus of national security and energy supply chains,” Whitman told the audience.

She said she was “excited to share some of our efforts to onshore and finance mineral projects in the midstream, especially through recycling and commercializing new energy storage technologies to strengthen our domestic supply chains and reduce influence from foreign adversaries”.

The United States, she said, is actively building new supply chains.

“The United States will continue to de-risk and diversify our supply chains to strengthen our economic security.”

But the primary goal remains securing resources for American industry.

“Our goal is to build secure and globally competitive mineral supply chains in America,” Whitman said.

Financing the Missing Middle

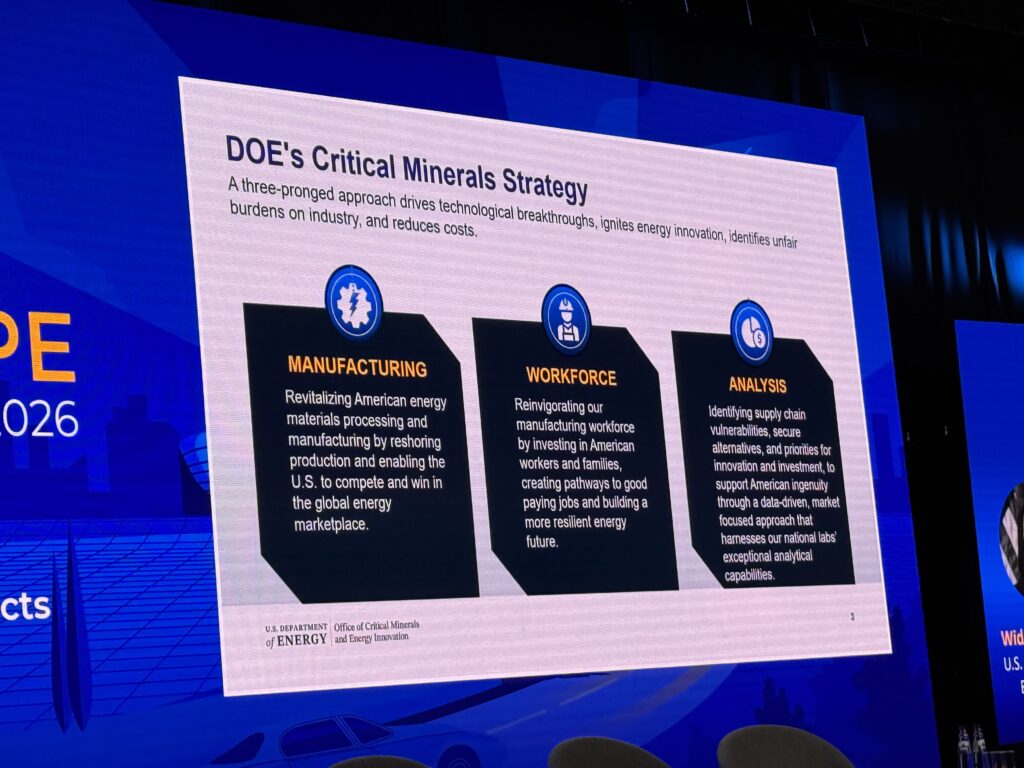

Whitman emphasised that the biggest challenge in mineral processing projects is not technology but financing.

“Commercializing these midstream technologies is not a technical issue, but more of an economics issue,” she said.

Projects often struggle to move from demonstration stage to full-scale production.

“In order to unlock downstream production of new innovative energy technologies, we need to capture that missing middle of mineral production,” Whitman said. “Otherwise, our deployment of advanced energy technology will not be successful.”

To solve that gap, the US Department of Energy is deploying a range of financial tools. “This includes supporting pilot and demonstration projects, fostering public-private partnerships, and identifying and resolving bottlenecks in the supply chain.”

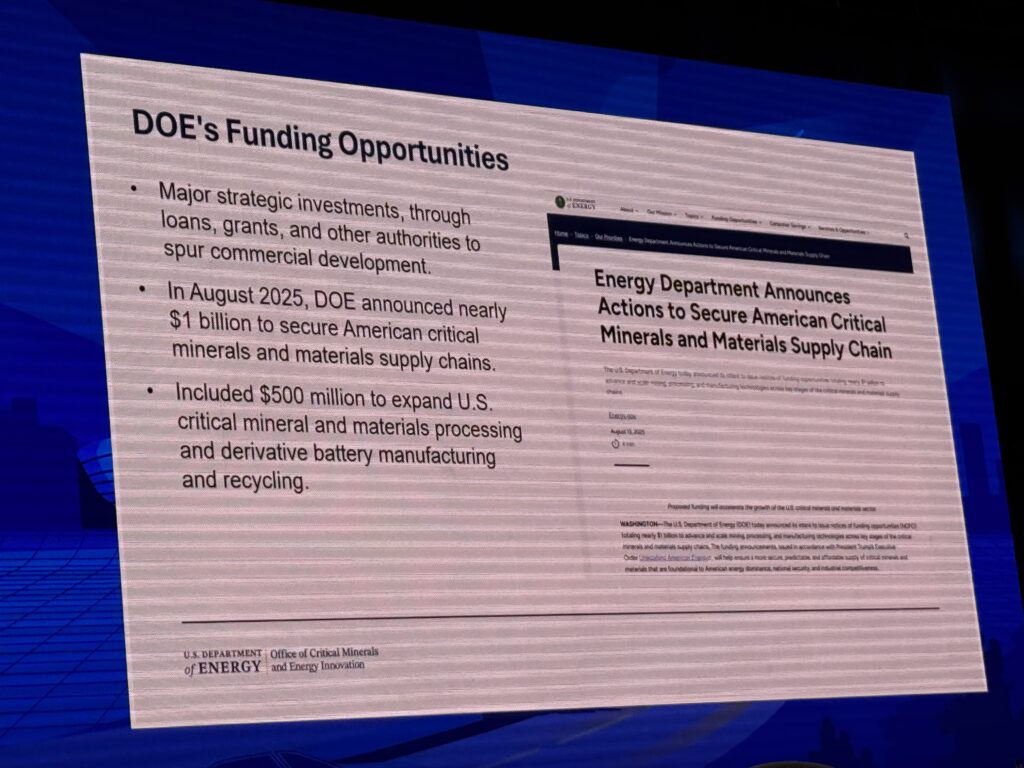

A Billion-dollar Funding Programme

Whitman highlighted nearly $1 billion in funding announced in 2025 to accelerate domestic mineral production and processing.

The funding program includes:

- Up to $135 million for projects demonstrating new rare earth refining technologies.

- Approximately $250 million for technologies that produce valuable mineral by-products from existing industrial facilities.

- Up to $500 million to expand critical mineral processing, battery manufacturing and recycling.

The aim is to move projects rapidly to commercial scale.

“Our goal is to not just produce materials, but to produce them at scale to meet the nation’s demand,” Whitman said.

Strict Rules to Exclude Chinese Influence

Projects receiving US funding must also comply with strict national security criteria.

“When we award funding for projects, we conduct due diligence to ensure US taxpayer money is not going to foreign entities of concern,” Whitman said.

The policy is designed to reduce dependence on Chinese supply chains. “We cannot win the race of reshoring and commercializing midstream mineral processing with continued reliance on China.”

A Global Competition for Supply Chains

Although Whitman emphasised cooperation with allies, her presentation made clear that Washington is actively building a global supply chain architecture aligned with US strategic interests.

“The US government is eager to collaborate with allies and partners to create secure supply chains that are free of foreign entities of concern,” she said.

Recent initiatives include a global critical minerals forum and new bilateral agreements.

“In February the Department of State hosted representatives of 54 countries and the European Commission for the Critical Minerals Ministerial,” Whitman said. “We signed 11 new bilateral frameworks and memorandums of understanding to build secure and resilient critical mineral supply chains.”

Europe’s Weak Points

When asked to identify the most fragile part of Europe’s supply chain strategy, panellists pointed to several structural weaknesses.

Muylle highlighted financing.

“The weak link is financing, the de-risking and making sure the business case is solved.”

Vanherberghen pointed to political hesitation.

“For me it’s the willingness of political stakeholders to support development of this industry.”

Conforti emphasised the impact of high energy costs.

“If you don’t fix energy prices, midstream cannot happen.”

The Strategic Race Has Begun

The Brussels discussions revealed a growing transatlantic competition over the future of mineral supply chains.

Europe recognises the strategic importance of critical materials but remains cautious about large-scale industrial policy. The United States has already begun deploying funding tools, diplomatic partnerships and regulatory conditions to reshape supply chains in its favour.

At the same time, both sides are responding to the same strategic reality. China still dominates large parts of the global mineral processing industry.

For European policymakers, the central question is no longer whether the competition exists. It is whether Europe can move fast enough to secure its own place in the emerging global architecture of critical mineral supply chains before others do.